Is Gap Cover Really Worth It in South Africa?

Gap cover bridges the shortfall between medical aid payouts and private hospital specialists' actual fees, protecting South African families from unexpected out-of-pocket costs.

- Who: Individuals and families on comprehensive medical aid plans.

- What: Covers co-payments, shortfalls, and non-tariff fees.

- When/Where: Available nationwide for in-hospital procedures.

- Why: Prevents financial strain and ensures full specialist access.

Compare gap cover options and get your free, no-obligation quote today.

The Shocking Truth About Your Medical Aid Claim Shortfalls

Many South Africans believe that having a medical aid plan means all private hospital bills are fully paid.You pay high monthly premiums for medical aid, expecting complete safety when it comes to paying medical costs.

But, you can still get a massive bill after a hospital stay.

This happens because doctors charge much more than the official rate the medical aid pays.

The only way to protect yourself from claim shortfalls and procedure co payments is by joining a solid Gap and Top up plan.

bestmedicalaid.co.za will explain how a Gap and Top Up plan protects your family from financial ruin.Let us explore how these policy benefits work and how you can choose the right plan for your needs and budget.

Why Medical Aid Alone is Not Enough

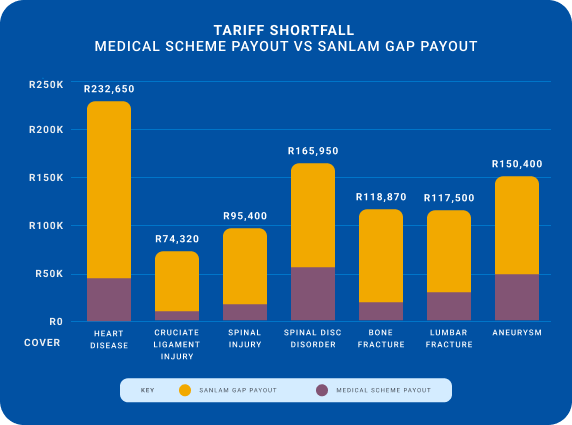

Medical aid schemes pay doctors according to a set price list called medical scheme tariff.

Medical aid schemes pay doctors according to a set price list called medical scheme tariff.However, private specialists often charge 5 times more than this standard rate.

If your doctor charges 500% of the rate, your medical aid only pays 100% and you must pay the remaining balance (medical shortfall) out of your own pocket.

It can be a significant shortfall, as a single day in intensive care can cost tens of thousands of Rands, and can result in great financial difficulty for you.

A Gap and Top Up plan is designed to pay these exact shortfalls by providing an extra safety net for you and your loved ones.

What is Gap and Top Up Cover?

A Gap and Top Up plan is an insurance policy, not a medical aid, so you must be a medical aid member for it to work.Your medical aid is governed by the Medical Schemes Act and pays for basic care and your normal hospital stays.

How It Differs From Medical Aid

Gap cover is short-term insurance governed by the Short-term Insurance Act and only pays the hospital bills that your medical aid does not cover.

A medical aid usually pays the hospital directly for your treatment, but Gap cover usually pays you the money, and you pay the provider.

The Core Focus of Zestlife

Zestlife is a top Gap Insurance provider in South Africa with plans that are designed to fit perfectly with all major medical scheme benefits.

No matter your base medical aid, Zestlife fills any payment holes, offering high payout limits and cover for a wide range of medical events.

Main Types of Gap and Top Up Plans

Gap and Top Up insurance plans offer different levels of cover, with most providers offering 3 main choices for you to consider.1. Essential Gap Cover

This basic policy option focuses mainly on in-hospital specialist and doctor shortfalls and pays up to an extra 500% of the medical scheme tariff.

It is ideal for healthy, younger people who want basic protection against sudden accident bills and keeps monthly costs low while covering the most common risks.

2. Comprehensive Top Up Plans

These are premium plans offering much wider protection, covering co-payments, (which are fixed fees you must pay before certain scans or procedures).

They also cover cancer treatment shortfalls once your medical aid limit is reached.

Many members choose this option for total peace of mind.

What Benefits Does Gap Cover Include?

Gap and Top Up plans, like Zestlife Gap Cover, include:Core Benefits

- Cover for medical expense shortfalls

- In-hospital and selected out-of-hospital procedures

- Payments above medical aid tariffs (often up to multiple times the rate such as 500%)

Additional Protection

- Hospital and scan co-payments Oncology-related shortfalls

- Pre- and post-surgery consultations Trauma and support benefits

Some plans even offer cover for:

- Accidental injury treatment

- International travel emergencies

- Additional cancer-related expenses

Key Benefits and Features to Compare

When deciding if you want to join, please compare these critical features.- Shortfall Cover Percentage:: Plans must pay at least 500% of the medical scheme tariff.

- Co-payment Benefit: Some medical aids require you to pay amounts towards specialist treatments like, R10,000 or more for an MRI scan.

A good gap cover policy pays this fee for you. - Sub-limit Increases: If your medical aid limits internal prostheses, like a new hip joint, gap cover can provide extra funds to meet that shortfall.

- Cancer Treatment Benefit: Cancer therapy is very expensive and a plan with a dedicated oncology top up is highly valuable.

- Casualty Unit Benefits: Some plans pay for emergency room visits after an accidental injury, even if you are not admitted.

Typical Costs and Benefits in 2026

In 2026, gap cover remains a highly affordable and valuable addition to medical aid.These assumptions are age dependent.

| Plan Level | Average Monthly Cost (2026) | Maximum Annual Benefit Limit |

|---|---|---|

| Basic Cover | R160 to R270 | R198,000 per person |

| Comprehensive Cover | R330 to R650 | R198,000 per person |

These low monthly rates make the extra cover highly cost-effective when compared to the potential cost you face with of short paid claims

So, is Gap Cover Worth It?

Most certainly, Gap cover is y worth it for medical aid members who:✔ Use expensive, private healthcare providers

✔ Have a hospital plan or lower benefit medical aid plan and are at risk of short paid claims

✔ Want comprehensive protection against large, unexpected hospital expenses

✔ Have dependants to cover

✔ Are concerned about oncology or expensive chronic illnesses

✔ There are plans with no waiting periods and no maximum entry or exit ages

Practical Tips When Using Your Gap/Top Up Plan

To get the most out of your plan, follow these simple steps:- Use Network Doctors: Many medical schemes currently have agreements with specific doctors and by using these network doctors you keep your initial shortfalls lower.

- Submit Claims Quickly: Most plans require you to submit claims within 6-months of your hospitalisation. Do not wait too long before submitting your claim..

- Keep All Documents: You will need your hospital account, the doctor's bill, and the medical aid statement.

- Use the Mobile App: Plans have apps that let you upload photos of your bills.

- Understand Your Waiting Periods: New policies usually have a standard 3-month general waiting period, but pre-existing conditions may have a 12-month waiting period.

But, every medical aid member should have a Gap Cover plan!

Healthcare costs are rising way faster than inflation and difference between medical scheme rates and specialists fees just increases over time.A Gap/Top Up plan will help you protect and extend your finances, prevent you going into medical debt and ensure you have access to quality private healthcare.

It is better to have the cover and not use it, than not have it and need it when you need it most.

Frequently Asked Questions: What is the Finest Gap Cover Plan?

1. Can I get gap cover if I do not have medical aid?

No, you cannot. Gap cover is designed specifically to pay the shortfalls left by a medical aid scheme. You must be an active member of a registered South African medical aid to qualify.

2. Will gap cover pay for my day-to-day doctor visits?

No, it does not. Gap cover is created to handle shortfalls from in-hospital procedures. It also covers specific out-of-hospital surgeries and selected scan co-payments. It does not cover routine GP visits or daily medicine.

3. Is there a maximum limit on what gap cover will pay?

Yes, there is a legal limit. By South African law, all gap cover policies are limited to a maximum payout. The current legal limit is set at R198,000 per insured person per calendar year. This legal limit is updated annually by the government.

4. Do waiting periods apply when I sign up?

Yes, standard waiting periods always apply to protect the fund. Usually, there is a three-month general waiting period for new members. For any pre-existing health conditions, you will have a twelve-month waiting period.

5. Can my whole family join under one policy?

Yes, most popular providers offer excellent family policies to their clients. A single family policy covers you, your spouse, and your registered dependents at a discount.

Get Your Free Quote

Talk to me — I am here to help you, at no charge.

Send me your questions and concerns. I'll answer them for you.

The plan works with any medical aid!

Enhance your cover without having to change from your medical scheme!

Note: Benefits are plan dependant. It is important to note that this product is specifically designed to help you meet the private tariffs charged by doctors, anaesthetists, radiologists, physiotherapists and specialist surgeons, for in-patient treatment. It does not cover the actual cost of the hospitalisation.No benefits are payable for a period of 12 months from the start date of cover in respect of medical conditions, for which in the 12 months before the start date of the cover, medical advice, diagnosis, care or treatment was received or would reasonably have been recommended. Pregnancy before the start date of cover will be regarded as a pre-existing condition and any pregnancy and birth related claims will be excluded for 12 months from the start date of the cover.

Terms and conditions do apply.

You must consult the schemes/company product brochures and rules for comprehensive benefit descriptions.

We will offer you the best help at no cost!

Easy-to-understand articles on medical aid.

![]() 083 655 2164

083 655 2164

You must consult the schemes/company product brochures and rules for comprehensive benefit descriptions.

![]() Medical aid pays healthcare costs.

Medical aid pays healthcare costs.

What if a disability stops your income?

Peter Pyburn - Authorised Financial Services Provider has been fully licensed to provide expert financial services since 1991.

Peter Pyburn - Authorised Financial Services Provider has been fully licensed to provide expert financial services since 1991.Based in Sandton, Johannesburg, Gauteng, we specialise in comprehensive financial planning including: Death and Disability Cover, Retirement Planning, Investment Strategies, Medical Aid, Estate Planning

FSP Licence 2995 and Medical Aid Accreditation BR 7428.

Why Choose Peter Pyburn?

Over 30 ears of experience in financial services - Fully Licensed and Accredited for medical aid and other Personalised financial advice.

![]() Council of Medical Schemes

Council of Medical Schemes

Medical Disclosure

By submitting an enquiry you agree to us collecting the information in the fields above. Please refer to our POPI Manual.

Your data will be processed according to the Protection of Personal Information Act (POPIA) guidelines.

Medical aid benefits are subject to change. Please consult the medical aid brochure and speak to bestmedicalaid.co.za before making any decisions.

South African rights reserved.